Farm Debt in 2026: How to Know If Your Borrowing Is Healthy (and How to Negotiate Better Terms)

The State of Farm Debt in 2026

Australian farm debt has climbed to record levels. Aggregate lending to the farm sector reached $142.5 billion in 2024-25, up 5% in real terms from the previous year. Grain-based enterprises account for roughly $56 billion of that total, with beef grazing and feedlot operations the next largest borrowers at around $35 billion.

Those numbers sound alarming in isolation. But context matters. About half of all broadacre farmers still carry little or no debt. The average equity ratio for broadacre and dairy producers hit 91% in 2023-24 - the second highest level in 25 years. Australian farmers, as a group, have never been wealthier in asset terms.

The problem is not debt itself. Debt is a tool. The problem is when debt servicing costs consume too much of your income, leaving no buffer for a poor season. With the RBA cash rate sitting at 4.10% and commercial farm lending rates around 5-6%, the cost of carrying debt is significantly higher than it was three years ago. That changes the maths on everything from land purchases to machinery upgrades to operating finance.

3 Ratios That Tell You If Your Debt Is Healthy

You do not need a finance degree to assess whether your borrowing is sustainable. Three ratios, all of which P2PAgri calculates automatically from your accounting data, give you a clear picture of your debt health. These are the same ratios your bank uses when assessing your business, so knowing them puts you on equal footing in any lending conversation.

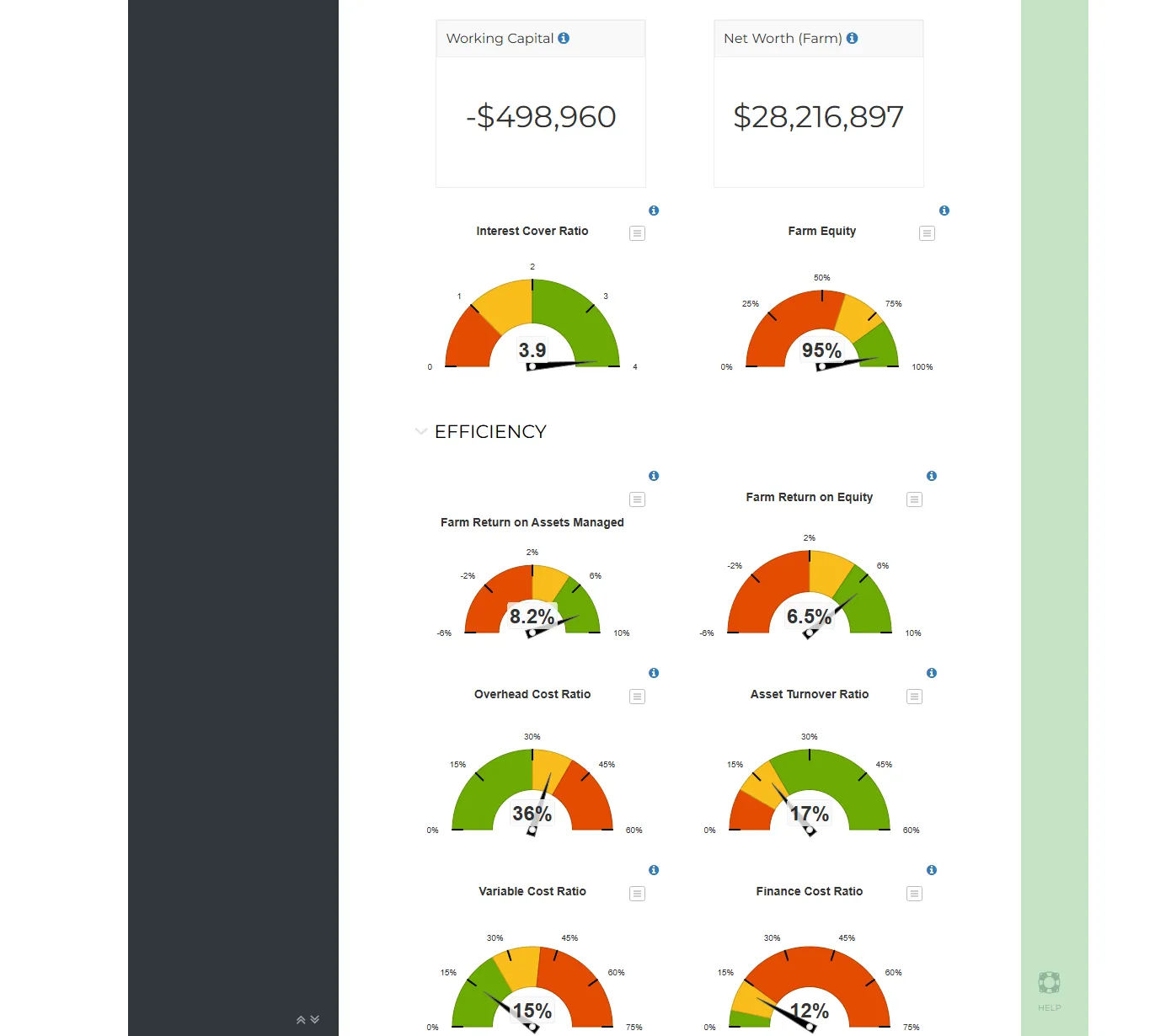

1. Equity Ratio

What it measures: how much of your business you own versus how much the bank owns. Calculated as total equity divided by total assets, expressed as a percentage.

Above 80% is strong. Between 60-80% is manageable but worth monitoring. Below 60% means you are highly leveraged, and any significant drop in land values or commodity prices could put you in a difficult conversation with your lender. As our benchmarking guide explains, the trend matters as much as the number. An equity ratio that has slipped from 85% to 75% to 68% over three years is telling you something important, even if 68% still looks acceptable on paper.

2. Debt Servicing Ratio

What it measures: how much of your gross farm income goes to interest and principal repayments. This is the ratio that determines whether your debt is comfortable or suffocating.

Below 20% is healthy for most farming operations. Between 20-25% is tight but workable if you have consistent income. Above 25% in a normal year means one poor season could create serious cash flow pressure. Above 30% is dangerous territory regardless of your equity position.

The farms that got into trouble during the 2017-2019 drought were not all bad operators. Many had simply accumulated debt servicing obligations that could not flex when income dropped. A $150,000 annual loan repayment is manageable when gross income is $1 million. It becomes crippling when a drought cuts that income to $400,000.

3. Interest Coverage Ratio

What it measures: how many times over your operating profit can cover your interest payments. Calculated as operating profit divided by total interest expense.

An interest coverage ratio above 3 means your business generates three times more profit than it needs to cover interest costs. That is comfortable. Below 2 means your margins are thin and you have limited room to absorb cost increases or income drops. Below 1 means your operating profit does not even cover your interest bill, and you are effectively borrowing to pay interest.

ABARES data shows the average interest coverage ratio for broadacre and dairy farms increased to 22% of gross income in 2023-24, well above the long-term average but still below the peaks seen in 2006-07. The proportion of farms facing financial stress from debt remains low at around 2%, but it has been trending upward.

When Debt Is Good: Leveraging for Growth

Not all debt is created equal. There is a meaningful difference between debt that funds productive assets and debt that papers over cash flow shortfalls.

Productive debt is borrowing that generates a return greater than its cost. Buying land that produces a 6% return on investment when your interest rate is 5% is productive debt. The asset generates enough income to service the loan and contribute to profit. Over time, as the loan is repaid and (assuming values hold) the asset appreciates, productive debt builds wealth.

Survival debt is borrowing to cover operating costs, repay existing loans, or fund living expenses during tough seasons. It does not generate any return. It simply adds to the servicing burden without improving the business's earning capacity. This is the type of debt that compounds into trouble.

The question is not whether you should borrow, but whether what you are borrowing for will generate enough additional income to comfortably cover the repayments - including in a below-average year. As we covered in our land purchase framework, modelling the investment decision with scenario analysis is the only reliable way to answer that question.

How to Negotiate Better Terms With Your Bank

Most farmers accept whatever their bank offers. That is understandable - the relationship feels important, and nobody wants to rock the boat. But banks are businesses too, and lending terms are negotiable. The difference between a good deal and a poor one can be tens of thousands of dollars per year.

Know Your Numbers Before the Meeting

The single most important thing you can do before a bank review is walk in with your own financial analysis already done. As our guide to getting the best deal from your bank explains, when you present your Management P&L, Balance Sheet, key bank ratios with trend charts, and scenario analysis showing how your business performs under different conditions, two things happen. You demonstrate professional management. And you control the narrative rather than reacting to whatever the bank presents to you.

Banks internally score every farm business on risk. The better your risk score, the more competitive the rate they can offer. Your job is to give them every reason to score you well: strong equity, manageable debt servicing, diversified income, and evidence that you have stress-tested your business against poor scenarios.

When to Ask

Timing matters. The best time to negotiate is when your business is performing well and you have options. Do not wait until you are under cash flow pressure to talk to your bank about terms - by then, your negotiating position is weak.

Annual review time is an obvious trigger, but you do not have to wait. If you have had a strong season, improved your equity ratio, paid down debt ahead of schedule, or received competing offers from other lenders, those are all legitimate reasons to start a conversation about your rate and fee structure.

What to Negotiate

Interest rate is the headline number, but it is not the only lever. Consider negotiating on line fees and ongoing management charges, which can add 0.3-0.5% to your effective rate. Ask about the structure of your repayments - principal and interest versus interest-only for a period may improve cash flow. Review whether a fixed rate on part of your borrowings provides better certainty, particularly if you are concerned about rate rises.

Also review your overall banking package. Many farmers have their lending, transaction accounts, insurance, and wealth management all with the same bank without ever questioning whether the bundled deal is actually competitive. Sometimes splitting services delivers a better overall outcome.

What Leverage You Have

If your equity ratio is above 70%, your debt servicing ratio is below 20%, and your business is profitable, you have leverage. The bank does not want to lose a good client. Be prepared to mention that you have explored other options - even if you have not formally applied elsewhere, knowing what competitors are offering gives you a reference point.

Agricultural lending is competitive. NAB, ANZ, CBA, Westpac, Rabobank, Bendigo Bank, and regional lenders all want the best farm clients. A well-presented business with strong fundamentals has more options than most farmers realise.

The $15,000 Interest Saving That Started With a P2PAgri Report

Tony Hudson from Hudson Facilitation, one of P2PAgri's accredited advisers, used P2PAgri to help a client who was seeking $1 million in additional borrowing for a farm expansion. Rather than approaching the bank with a verbal pitch and a set of tax returns, Tony prepared a full financial package: Management P&L, Balance Sheet, key bank ratios with trend charts, cash flow projections, and scenario analysis showing how the business would perform under good, average, and poor seasonal conditions.

The bank was so impressed with the quality of the presentation that they offered a 0.5% interest rate reduction on the entire lending facility, not just the new loan. On $3 million in total borrowings, that 0.5% equates to $15,000 per year in interest savings. Over a 10-year loan term, that is $150,000 - from a single well-prepared bank meeting.

The lesson is straightforward. Banks price risk. When you reduce their perceived risk by presenting comprehensive, well-structured financial data that shows you understand your own business, they respond with better pricing. The cost of preparing that data in P2PAgri is a fraction of the savings it can generate.

RIC Concessional Loans: Who Qualifies and How to Apply

The Regional Investment Corporation (RIC) offers concessional loans to eligible farm businesses at rates significantly below commercial lending. As of February 2026, the RIC farm business loan rate is 5.18%, held steady for a further six months. While this rate is set based on the average 10-year government bond rate rather than the RBA cash rate, it often comes in below what commercial banks offer.

RIC loans have several features that make them attractive. There are no application fees, no ongoing management fees, and no penalty for extra or early repayment. The standard term is 10 years with interest-only repayments for the first five years, followed by principal and interest for the remaining five. That interest-only period can be a significant cash flow advantage in the early years of a major investment.

Eligibility is focused on farm businesses and farm-related businesses facing financial impacts from events outside their control - drought, natural disaster, biosecurity risks, or market closures. RIC currently has $464.9 million in available funding for new loans in the 2025-26 financial year, with an additional $1 billion committed for loans beyond that period.

If you are considering an RIC loan, your application will need to demonstrate your financial position, the purpose of the borrowing, and your capacity to service the loan. Having your P2PAgri reports ready - including cash flow projections showing how the loan fits into your five-year plan - strengthens your application considerably.

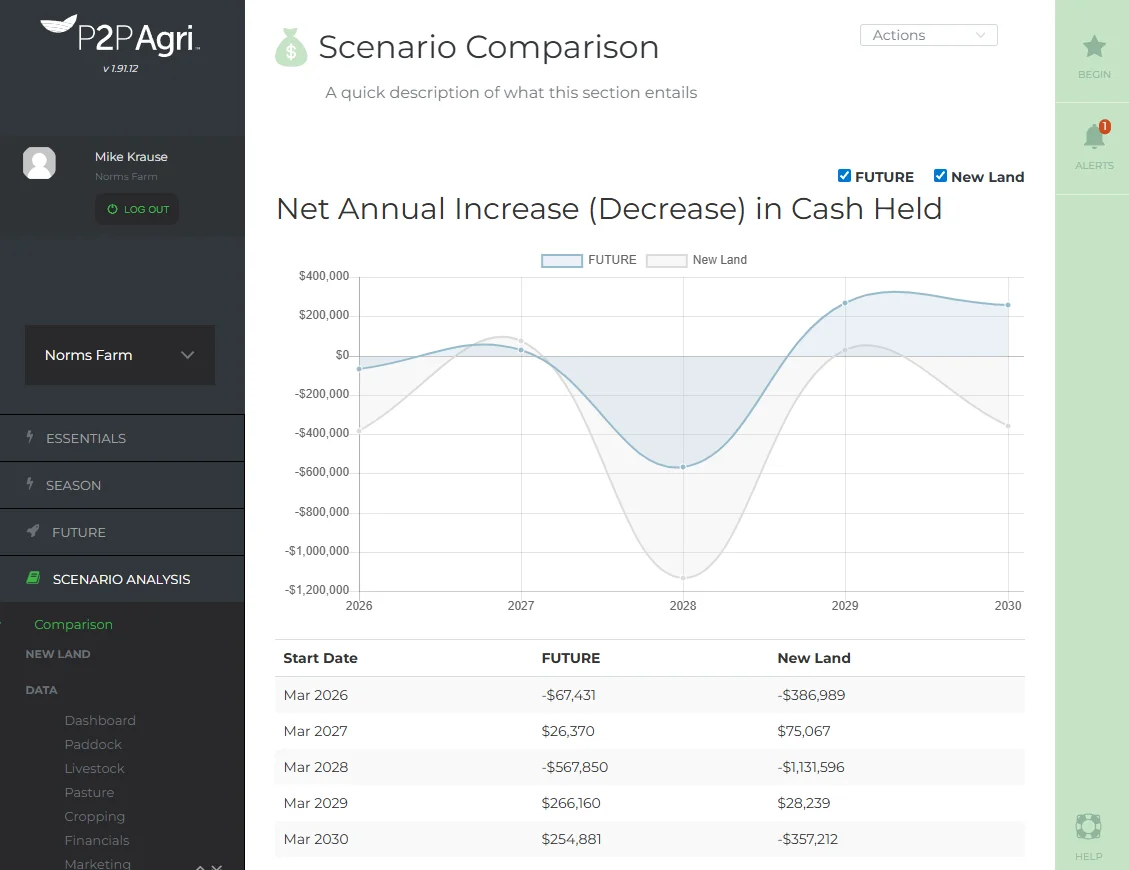

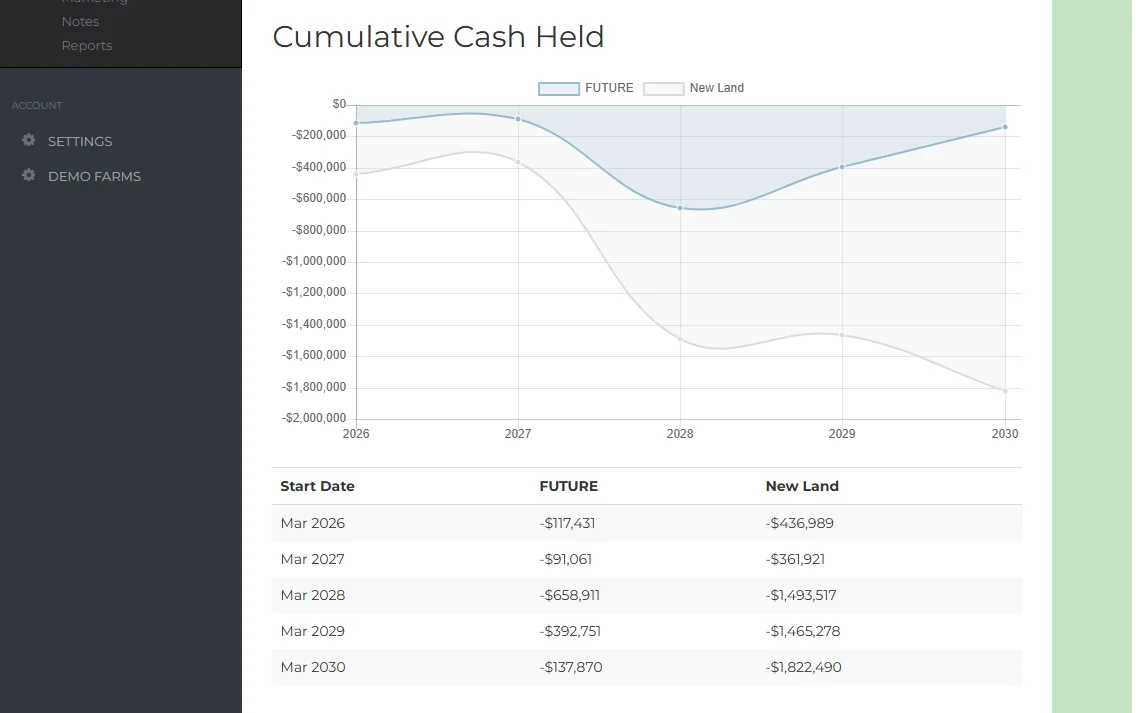

Using Scenario Analysis to Stress-Test Your Debt

Your bank is already thinking about what happens to your business if interest rates rise, if you get a drought, or if commodity prices fall. You should be thinking about it too - and you should be the one presenting that analysis, rather than waiting for your bank to raise concerns.

P2PAgri's Scenario Analysis lets you model these situations in minutes. Clone your current Future plan and adjust the variables: what happens if interest rates rise 1%? What about 2%? What if you get a decile 2 season in year two while carrying the higher rate?

The comparison view puts your baseline and stress-tested scenarios side by side across every financial metric for up to five years. You can see exactly how your cash flow, debt servicing ratio, and equity position change under each set of assumptions.

This is not just about satisfying your bank. It is about making better decisions for your own business. When you can see that a 1% rate rise increases your annual debt servicing by $30,000 but your business still generates positive cash flow, that is reassuring. When you can see that a 2% rise combined with a poor season would push your debt servicing ratio above 30%, that is a signal to either reduce debt, restructure repayments, or build a larger cash buffer before rates move.

What to Do Next

If you are carrying farm debt - and roughly half of Australian broadacre farmers are - the single most valuable thing you can do is understand exactly where you stand. Not approximately. Not based on a gut feel from last season. But with actual numbers that show your equity ratio, debt servicing ratio, and interest coverage right now, and how those numbers have been trending.

P2PAgri's free Essentials plan generates your Management P&L, Balance Sheet, and key bank ratios with visual dials and trend charts directly from your Xero or MYOB data. It takes about 15 minutes to sync your data and see where you stand. That is your starting point.

If you want to stress-test your debt under different interest rate scenarios, model the impact of paying down debt faster, or prepare a comprehensive financial package for your next bank review, the Future plan adds five-year projections, scenario analysis, and the comparison tools that make this possible.

And if you would rather have someone walk you through it, our network of accredited advisers work with farmers across Australia to review debt structures, prepare bank presentations, and negotiate better lending terms. It is worth a conversation.

Put This Into Practice

P2PAgri helps you apply these concepts with interactive tools and real-time analysis of your farm data.

Get Started Free