Should You Buy That Farm Next Door? A Financial Framework for Land Purchase Decisions

The Land Next Door Comes Up for Sale. Now What?

It is one of the biggest financial decisions a farming family will ever face. The block next door is on the market. It would fit perfectly into your operation. You could run it with existing machinery, spread your overheads across more hectares, and consolidate your position in the district. The agronomic case writes itself.

But the financial case is a different story. Australian farmland closed 2025 at a national median of $10,979 per hectare - nearly triple what it was in 2010. In Western Australia, values jumped 30% in a single year. In South Australia, they rose 25%. The maths of buying land has changed dramatically, and what made sense a decade ago may not stack up today.

The danger is not that farmers buy land. The danger is that they buy land based on emotion and opportunity without running the numbers first. As the GRDC's Farming the Business manual emphasises, every major business decision should be tested against the three pillars of farm financial health: liquidity, efficiency, and wealth. A land purchase that strengthens one pillar while destroying another is not the bargain it appears.

The 5 Financial Questions Before You Sign Anything

Before you call the agent, before you talk to the bank, and definitely before you shake hands at the clearing sale, you need honest answers to these five questions. Each one can be modelled in P2PAgri's Scenario Analysis, and each one has the potential to change your decision.

1. Can You Service the Additional Debt?

This is the question that matters most and gets answered least. Not "can the bank lend you the money" - banks will often lend more than is prudent - but "can your business comfortably service the repayments in a below-average year?"

The debt servicing ratio measures how much of your gross farm income goes to interest and principal repayments. A healthy farm business keeps this below 20-25%. Once it creeps above 30%, a single poor season can create serious cash flow pressure. The farms that got into trouble during the 2017-2019 drought were not necessarily bad operators. Many had simply over-committed on debt servicing relative to their income variability.

Calculate your current debt servicing ratio. Then calculate what it becomes with the new loan added. If it pushes past 25% in a normal year, proceed with extreme caution. If it exceeds 30%, the purchase is probably too aggressive regardless of the land quality.

2. What Happens to Your Cash Flow in Year One?

Land purchases create an immediate cash flow crunch. You have the deposit, stamp duty, legal costs, and potentially fencing, water infrastructure, or soil amendments before the block produces a dollar of income. If it is cropping country, you are funding a full season of inputs before seeing any return. If it is grazing country, stocking takes time and capital.

The critical metric here is your minimum cash balance over the first 12 months after settlement. If your cash flow projection shows you dipping below a comfortable operating buffer - or worse, needing an overdraft extension - the timing may be wrong even if the long-term economics work.

3. What Return Will the Land Generate Compared to Its Cost?

This is where many land purchase decisions fall apart under scrutiny. If you are paying $10,000 per hectare for country that generates $400/ha in gross margin, your return on that investment is 4% before overheads. That might be acceptable if interest rates are 3%, but with farm lending rates sitting around 5-6%, you are paying more to borrow than the land earns.

The return on assets managed ratio (operating profit divided by total assets) is your guide here. Research from Pinion Advisory shows that Australia's top 20% of grain farms achieve return on assets above 5%. If the new land dilutes your return on assets below your cost of borrowing, you need to be very clear about why you are still buying. Capital gain expectations alone are not a business plan.

4. What Does Your Equity Position Look Like After the Purchase?

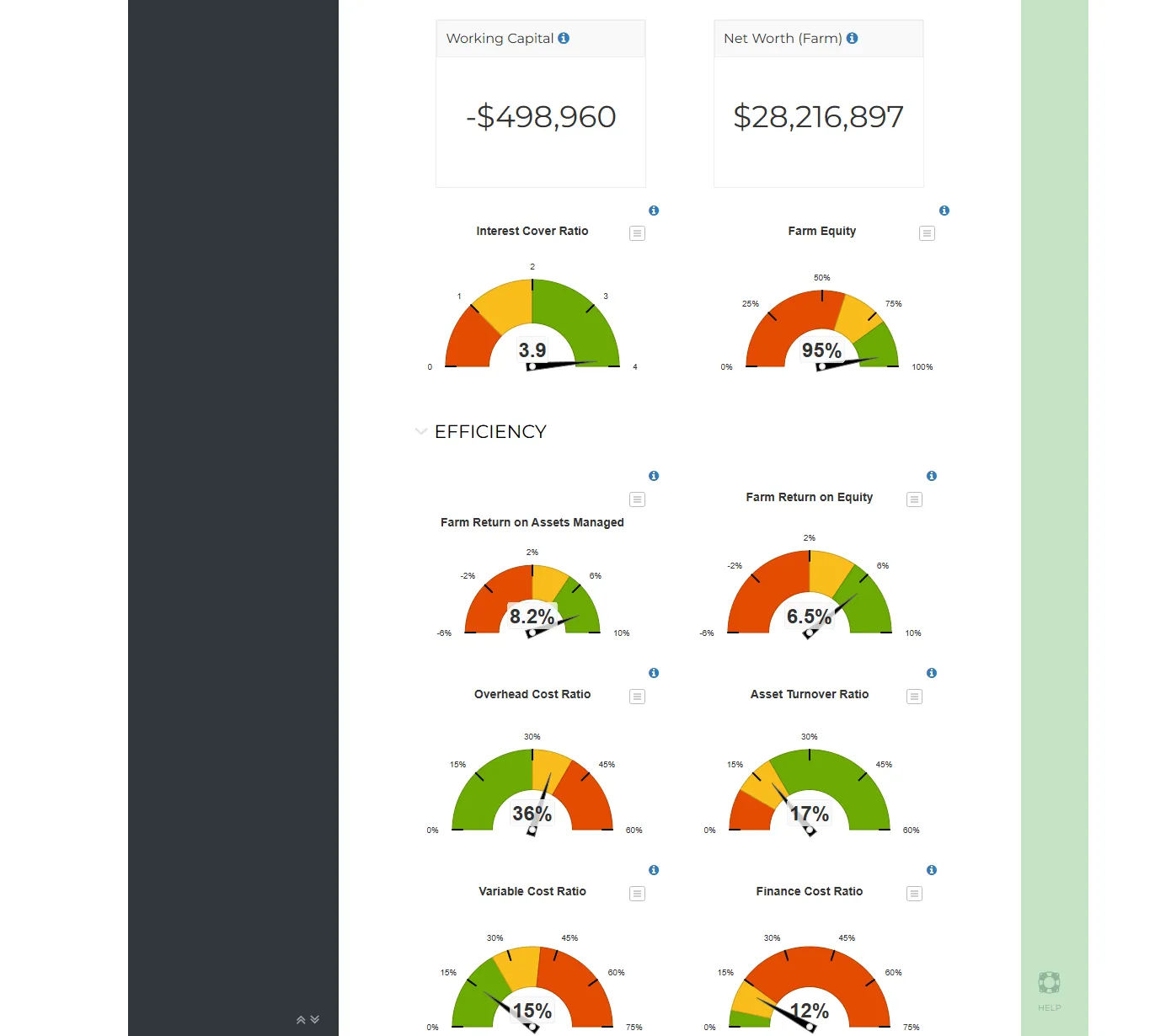

Your equity ratio - total equity divided by total assets - is the ratio banks look at first. A strong equity position (above 80%) gives you resilience and negotiating power. A weakened equity position (below 60%) makes you vulnerable to any downturn in land values or commodity prices.

If the land purchase drops your equity ratio from 85% to 65%, you have fundamentally changed the risk profile of your business. You have gone from a position of financial strength to one where a 15-20% drop in land values could put you in uncomfortable territory with your bank. This does not mean you should never buy, but you need to understand the trade-off.

5. What If Things Go Wrong?

Every land purchase decision should be stress-tested against a poor scenario. What if you get a decile 2 season in year two of ownership? What if commodity prices drop 20%? What if interest rates rise another 1%?

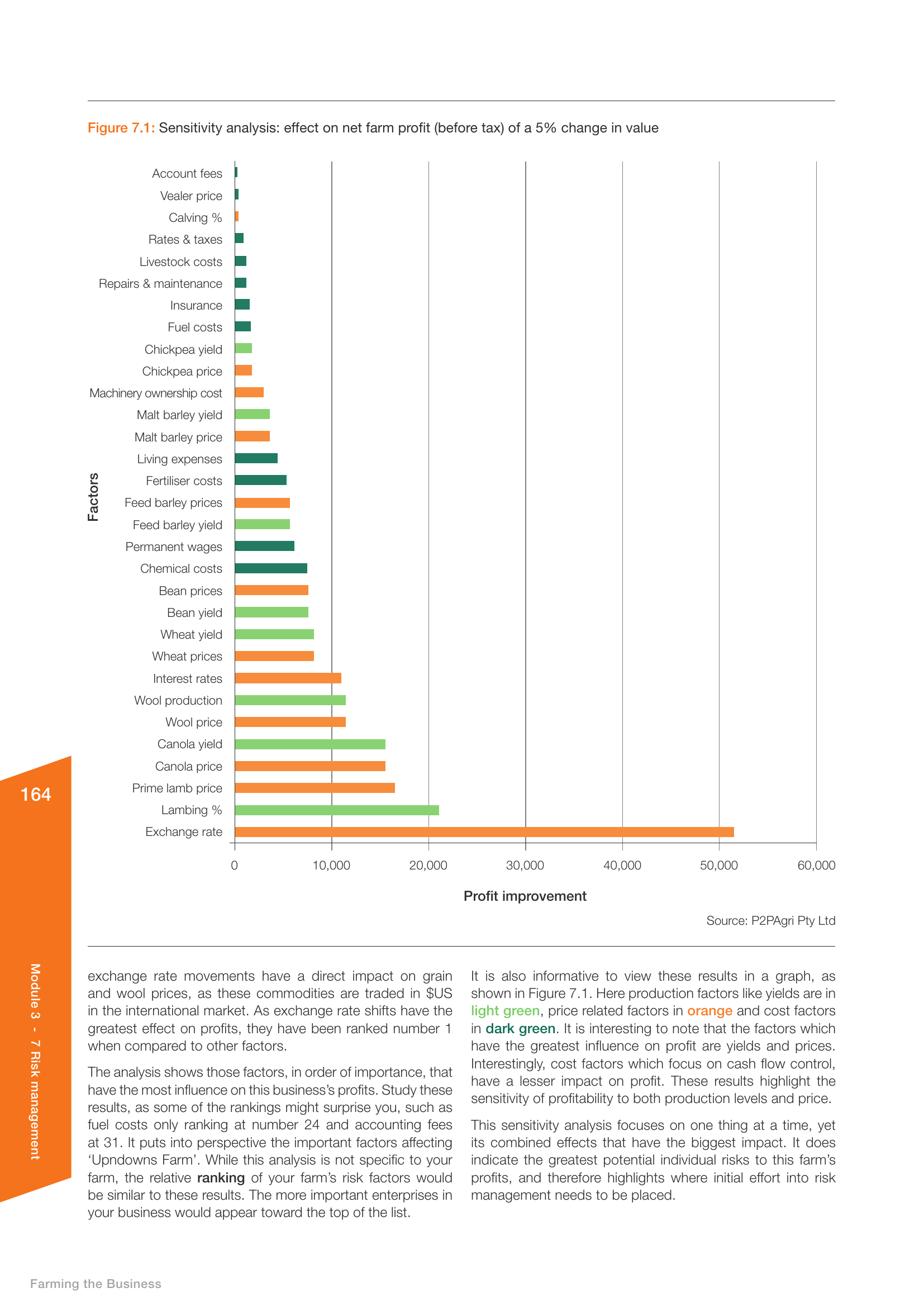

As the Farming the Business manual's section on sensitivity analysis makes clear, the factors with the greatest impact on farm profit are often the ones you control least: commodity prices, yields, and exchange rates. A land purchase that works beautifully in an average year but forces you to sell stock or restructure debt in a poor year is a purchase that has not been properly tested.

How to Model a Land Purchase in P2PAgri

P2PAgri's Scenario Analysis was built for exactly this type of decision. Here is how to set up a land purchase scenario and compare it against your current position.

Step 1: Get Your Baseline Right

Start with your current Future plan in P2PAgri. This is your "do nothing" scenario - your business as it stands today, projected forward over the next five years. If your baseline is not up to date, sync your Xero or MYOB data first so you are working from real numbers, not estimates.

Step 2: Clone and Create Your Land Purchase Scenario

Clone your Future plan to create a new scenario. This gives you an exact copy of your current business as a starting point. Then add the land purchase details:

On the balance sheet: add the land as a new asset at the purchase price. Add the corresponding loan (most include funding stamp duty and settlement costs) as a new liability with the correct interest rate, term, and repayment structure.

On the cash flow: the deposit, stamp duty, and legal costs should appear as outgoings in the settlement month. Loan drawdown appears as an inflow. Monthly or quarterly repayments flow through as ongoing outgoings.

On the P&L: add the expected income from the new country (cropping gross margins, livestock returns, or lease income if you are leasing part of it out). Add any additional variable costs - seed, fertiliser, fuel, and labour for the extra hectares.

Step 3: Compare the Two Scenarios Side by Side

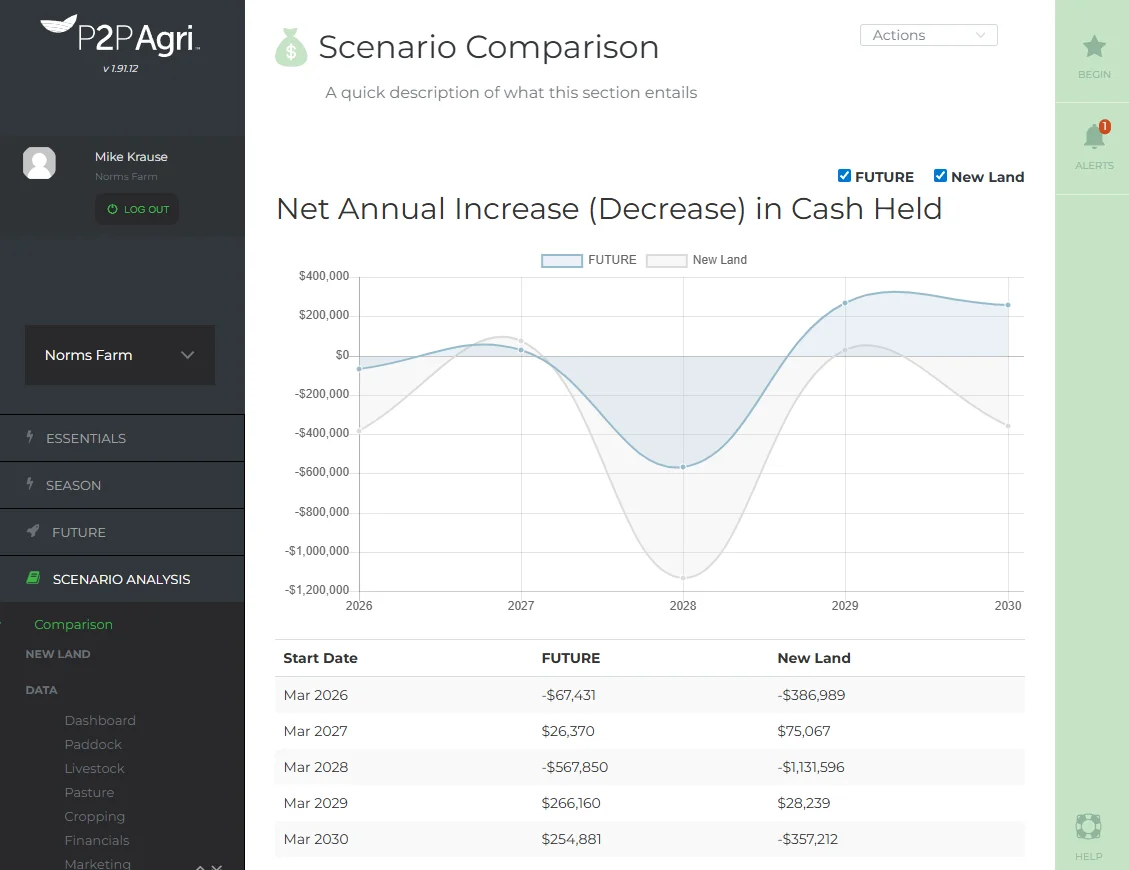

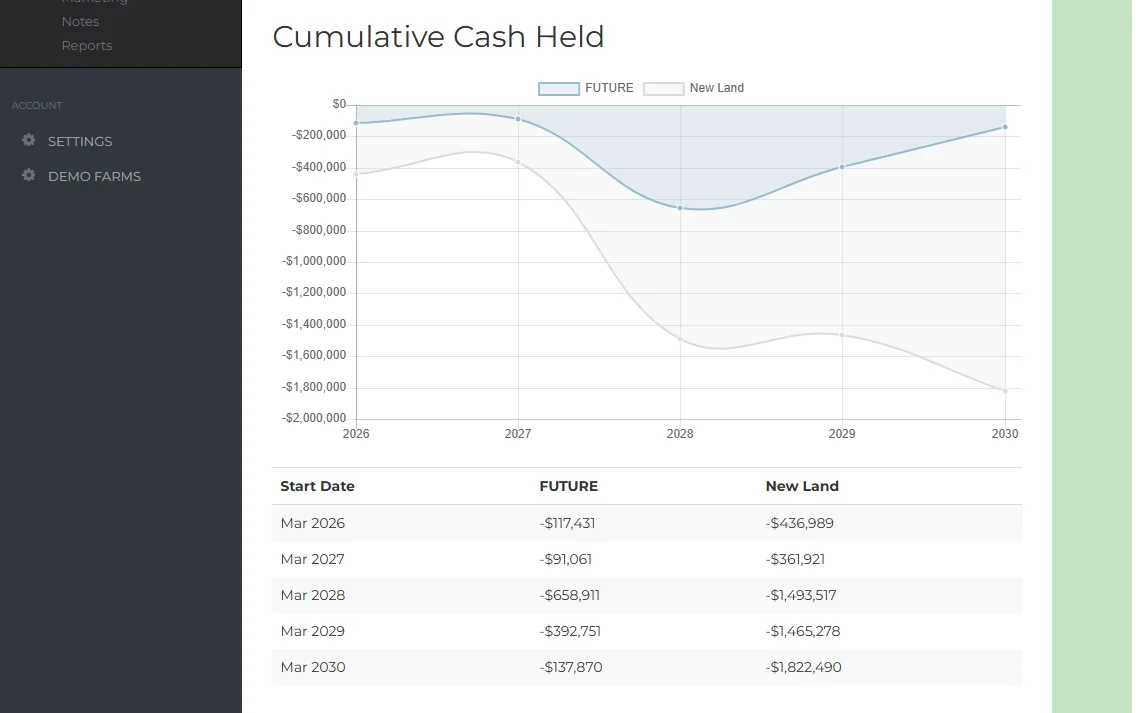

This is where the picture becomes clear. P2PAgri's comparison view puts your baseline ("Future") and your land purchase ("New Land") scenario side by side across every financial metric for up to five years. You can see immediately:

How does net cash held change year by year? What happens to net profit before tax? How do the key bank ratios (equity, debt servicing, return on assets) compare between the two paths?

The comparison chart above tells a story that spreadsheets struggle to show. You can see the initial cash flow hit of the purchase, the recovery period as the new land starts generating income, and whether the two scenarios converge or diverge over the five-year horizon.

Step 4: Stress-Test With a Bad Year

Clone the land purchase scenario again and model a drought or price shock in year two or three. Drop your yields by 30-40%. Cut commodity prices by 20%. See what happens to your cash flow, debt servicing ratio, and minimum cash balance. This is the scenario your bank will be thinking about even if they do not say it out loud.

If your business can absorb a poor year with the new debt and still meet all repayment obligations without selling core assets, the purchase is financially resilient. If it cannot, you need a contingency plan or a different deal structure.

A Case Illustration: $2M Purchase, $1.5M Borrowed

To make this concrete, consider a typical expansion scenario for a broadacre farm in southern Australia.

The opportunity: 400 hectares of cropping country adjacent to an existing 2,000-hectare mixed farm. Asking price is $2 million ($5,000/ha). The farmer has $500,000 in available cash and will borrow $1.5 million at 5.5% over 15 years with principal and interest repayments.

The numbers before the purchase: the existing farm generates average gross farm income of $1.2 million, operating profit of $350,000, and has total assets of $8 million with $1.5 million in existing debt. Equity ratio sits at 81%. Debt servicing ratio is 12% of gross income. Return on assets is 4.4%.

The numbers after the purchase (average year): the extra 400 hectares add approximately $280,000 in gross income and $180,000 in variable costs, contributing around $100,000 to gross margin. However, the new loan adds approximately $147,000 per year in repayments (principal and interest). Total assets rise to $10 million. Total debt rises to $3 million. Equity ratio drops to 70%. Debt servicing ratio climbs to 18%.

In a poor year: if gross income drops 30% across the whole farm (a realistic drought scenario), debt servicing ratio jumps to 26%. The farm is still solvent but cash flow is extremely tight. There is no buffer for unexpected expenses, and the bank will be watching closely.

The five-year view: if the farm strings together three average-to-good years, the additional income from 400 hectares progressively reduces the debt burden and the equity ratio recovers toward 75%. By year five, the expanded farm is in a stronger position than the original. But if a drought hits in year two, the business faces 18-24 months of severe cash pressure before recovering.

This is the kind of analysis that changes decisions. Not because the answer is always "don't buy" - often it is "buy, but structure it differently."

Red Flags That Say "Don't Buy"

Even when the land is agronomically perfect, the financial case sometimes says no. Here are the warning signs to watch for in your scenario analysis:

Your debt servicing ratio exceeds 25% in a normal year. This leaves no room for a poor season. One bad year could force asset sales or emergency refinancing.

Your equity ratio drops below 60%. You are now highly leveraged. Any decline in land values or sustained low commodity prices puts your entire business at risk, not just the new purchase.

The land's return does not cover its borrowing cost. If you are paying 5.5% on the loan and the land generates a 3% return on investment, you are going backwards every year. Capital gains might eventually bail you out, but banking on land price appreciation is speculation, not business planning.

Your cash flow shows negative months in the first two years without an overdraft buffer. If you need to extend your overdraft just to get through the first couple of seasons, the purchase is under-capitalised.

You cannot survive a stress-tested poor year without selling core assets. If your drought scenario requires selling breeding stock, machinery, or other land to stay afloat, the purchase is too aggressive for your current position.

The Alternative: Leasing vs Buying

Buying is not the only way to farm more country. Leasing offers a way to capture the production benefits of additional hectares without the capital commitment and debt risk of purchasing. It is worth modelling both options in P2PAgri before committing to either.

The key comparison points between leasing and buying are straightforward. Buying builds equity over time as you repay the loan and (assuming values hold) benefit from capital appreciation. But it concentrates risk. A lease preserves your equity ratio and cash reserves, giving you flexibility to walk away if conditions deteriorate. However, you do not build equity in the land, and you are exposed to lease renewal risk and potential rent increases.

As the GRDC's leasing and share-farming fact sheet outlines, the decision between leasing and buying often comes down to where you are in your farming career, your current debt position, and your appetite for risk. A younger farmer building equity might prioritise buying. An established farmer with existing debt might find leasing gives a better risk-adjusted return.

In P2PAgri, you can model both options as separate scenarios and compare them directly. Create one scenario with the land purchase and loan, and another with a lease arrangement showing the annual lease cost as an expense but no asset or liability on the balance sheet. The five-year comparison will show you which path produces better cash flow, which builds more equity, and which carries less risk.

What Your Bank Wants to See

If you are borrowing to buy land, your bank will assess the proposal against their lending criteria. Walking into that meeting with your own analysis already done - rather than waiting for the bank to tell you what they think - puts you in a fundamentally stronger position.

As we covered in our guide to getting the best deal from your bank, presenting a well-structured business case with scenario analysis is what separates farmers who get approved quickly at competitive rates from those who face weeks of back-and-forth and higher margins.

The information your bank will want to see for a land purchase application includes your current Management P&L and Balance Sheet, your projected cash flow including the new loan repayments, your key bank ratios (equity, debt servicing, return on assets) both before and after the purchase, a scenario comparison showing the baseline versus the purchase, and a stress-test showing the business can service the debt in a poor year.

P2PAgri generates all of these from your data. Tony Hudson from Hudson Facilitation, one of P2PAgri's accredited advisers, has used this approach to help clients secure favourable lending terms. When a farmer presents their own detailed financial projections showing they have stress-tested the decision, banks respond differently than when a farmer simply says "I want to buy the block next door."

Making the Decision

The purpose of this framework is not to talk you out of buying land. Farm expansion through land purchase has built some of Australia's most successful farming businesses. The purpose is to make sure you go in with your eyes open, with real numbers rather than rough estimates, and with a clear picture of both the upside and the risks.

The farmers who get land purchase decisions right are the ones who can answer "yes" to three questions. Can I service the debt in a poor year? Does my equity position remain resilient? Does the land generate a return that justifies the investment over time?

If the answer to all three is yes, you have a strong case. If one or more is no, it does not necessarily mean you walk away - but it does mean you need to restructure the deal, negotiate a different price, or consider leasing instead.

P2PAgri's Scenario Analysis lets you test all of this before you commit. Clone your current plan, add the land purchase, model the good years and the bad years, and see exactly how it changes your cash flow, P&L, and balance sheet for the next five years. That is what the tool was built for.

If you want help modelling a specific land purchase decision, our network of accredited advisers can walk you through the process. Or start with the free Essentials plan to get your current financial position established, and upgrade to the Future plan when you are ready to run scenarios.

Put This Into Practice

P2PAgri helps you apply these concepts with interactive tools and real-time analysis of your farm data.

Get Started Free