Farm Business Plan Template: What to Include and Why Your Bank Will Thank You

Why Every Farm Needs a Business Plan (and Why a Spreadsheet Is Not One)

Walk into any bank in regional Australia and ask what they want from farming customers in 2026, and you will hear the same answer: a current business plan. Not a tax return. Not a paddock book. A forward-looking plan that shows where the business is going, what it will cost to get there, and what happens if conditions change.

The trouble is that most Australian farms still do not have one. ABARES data shows that only around 36% of farm businesses engage with formal financial planning tools, despite over half of farm owners expecting to retire in the next 10 years and average farm debt now sitting at $142.5 billion nationally. The gap between what banks expect and what farmers typically present is wide, and it is closing slowly.

A business plan is not a spreadsheet of last year's numbers. It is not a list of paddock yields. It is not the budget you put together for your accountant in July. A real farm business plan is a living document that links your goals, your financial position, your seasonal operations, and your long-term forecasts into one coherent picture. When done well, it tells anyone reading it - your bank manager, your business partner, the next generation, or yourself - exactly what the business is, where it is going, and how it will get there.

The good news is that you do not need a 60-page document to do this well. You need the right structure, the right numbers, and a process that lets you update the plan as the season unfolds. The framework below covers what a modern Australian farm business plan should include, what your bank actually wants to see, and how to build it without spending months on a project that ends up in a drawer.

The 7 Sections Every Strong Farm Business Plan Includes

A complete farm business plan covers seven sections. Each one answers a specific question that a bank, partner, or adviser will ask. Skip any of them and you leave a gap that will get noticed.

1. Executive Summary

One page, written last. The executive summary tells the reader what the business is, who runs it, what you are asking for (a loan extension, capital for an expansion, a finance review), and the headline numbers that justify the request. If a bank manager only reads this page, they should still understand the shape of your business and the decision in front of them.

Strong executive summaries lead with the result. "Our 2,000-hectare mixed enterprise generated $480,000 net profit in 2024-25 with a 78% equity ratio. We are seeking a $1.5M facility to fund a neighbouring land purchase that lifts our 5-year forecast profit by an average of $145,000 per year." That is one sentence that sets up the entire conversation.

2. Business Overview

Who you are, what you do, and how the business is structured. This section covers ownership (sole trader, partnership, company, trust), key people and their roles, location and farm size, the enterprises you run (cropping, livestock, mixed), and any off-farm activities or investments. It should also cover succession status: is the next generation involved, what is the long-term ownership plan, and are there any pending transitions?

As our family farm as a business article explores, the structure of the family business often shapes every other decision. Banks and advisers need to understand who owns what and who decides what before they can usefully engage with the rest of the plan.

3. Financial Position

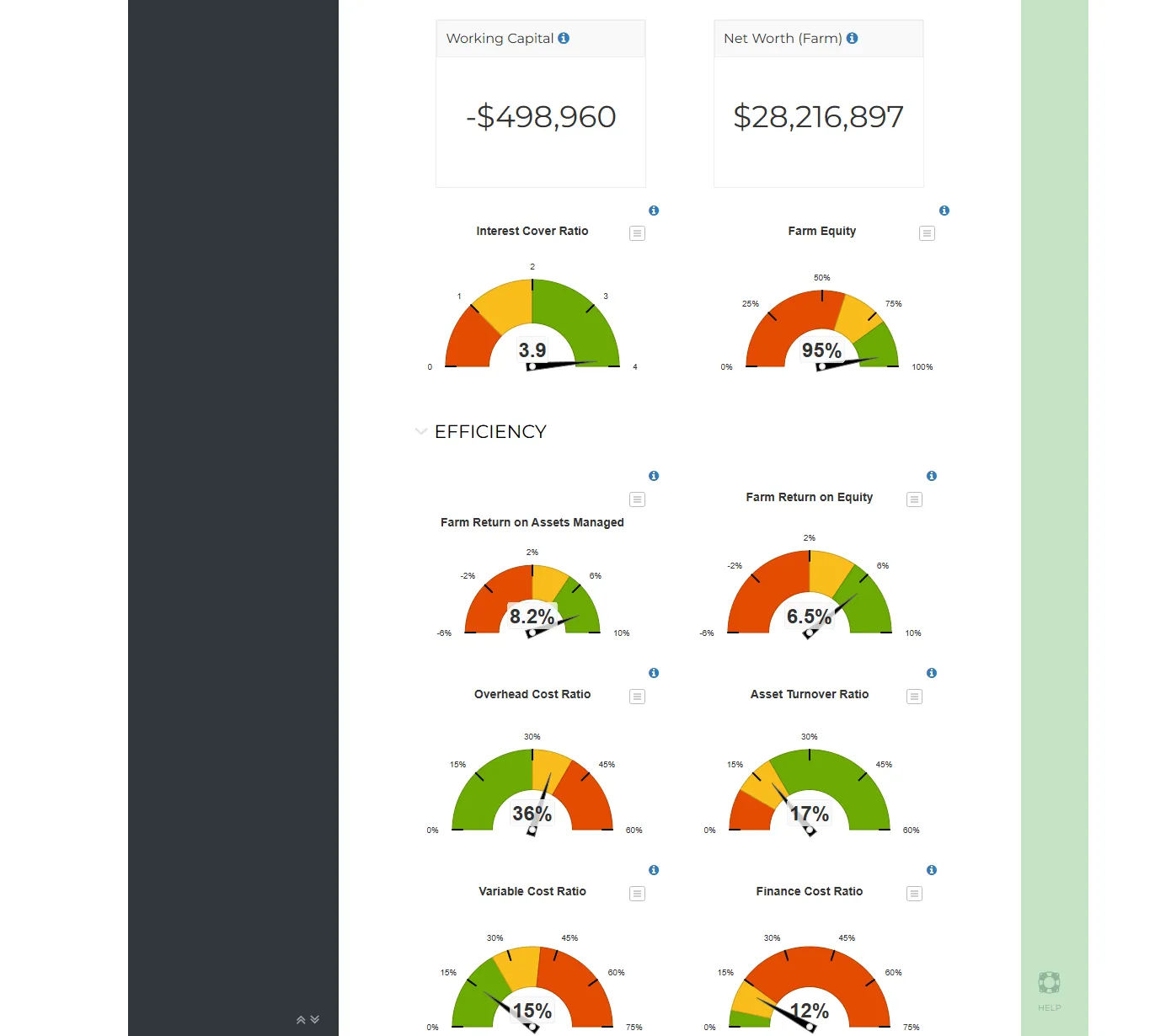

A current snapshot of the balance sheet: assets, liabilities, and equity. This is the section banks read most carefully because it tells them the security available, the debt currently outstanding, and the equity position underpinning any new lending. It should include land and buildings at current market valuation (not historical cost), plant and equipment at written-down value, livestock and grain on hand, receivables and payables, and a complete debt schedule showing each facility, its balance, interest rate, and maturity.

The key ratios sit here too. Equity ratio, debt servicing ratio, interest coverage, and current ratio. As our farm debt guide explains, these ratios are what every bank uses to assess your borrowing health. Including them in your plan, with a clear note on whether they are healthy, marginal, or stretched, demonstrates that you understand the same language your lender does.

4. Cash Flow Projections

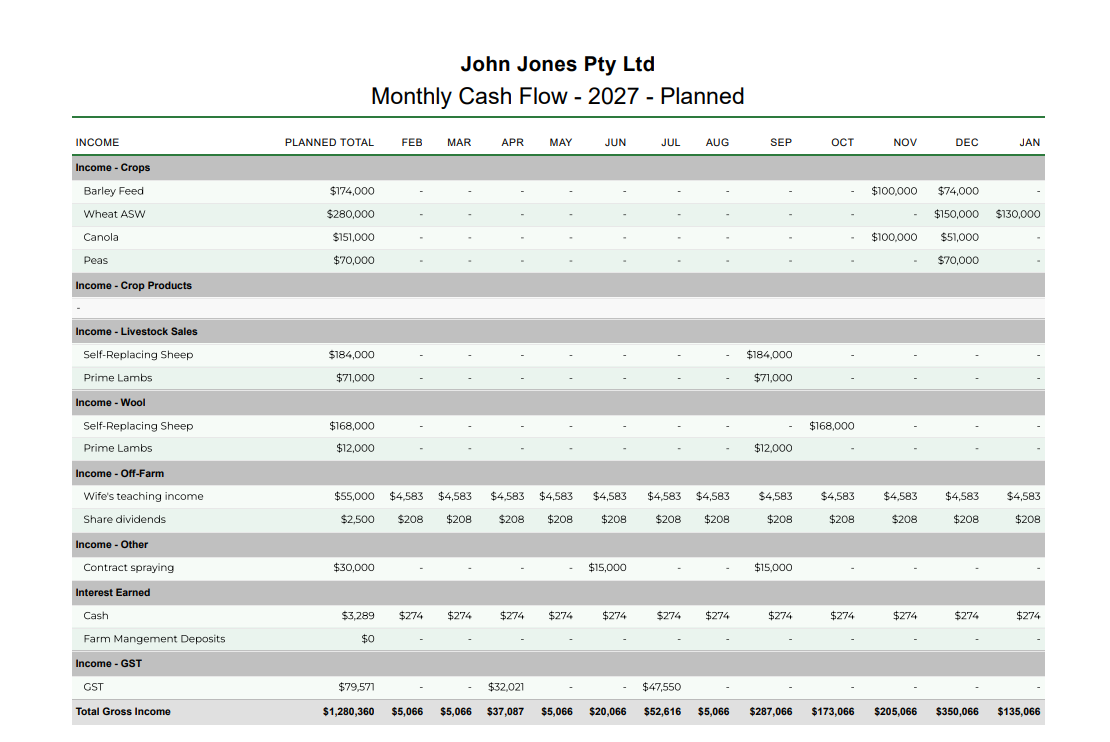

Monthly cash inflows and outflows for the coming season, showing opening balance, receipts (commodity sales, livestock sales, off-farm income, government payments), payments (variable costs, overheads, finance, capital, drawings), and closing balance. The projection should run a minimum of 12 months and ideally show seasonal variation through the calendar year.

This is where banks see whether you can actually service your debt month by month, not just on paper at year end. A business that finishes the year with $200,000 net profit but goes $400,000 overdrawn in September during peak input spending still has a problem. The cash flow projection forces that reality into the open and gives you the opportunity to plan facility limits, seasonal finance, or commodity pre-sales accordingly.

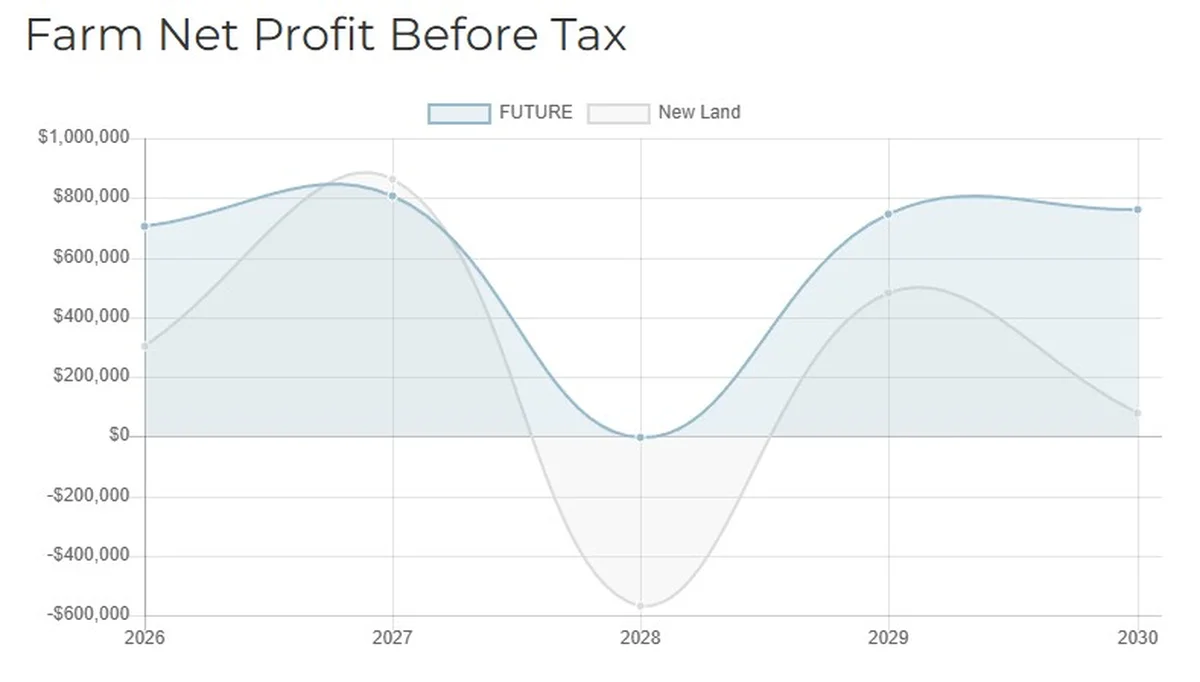

5. 5-Year Financial Forecast

A multi-year projection showing the management profit and loss, balance sheet, and cash flow over the next five years. This is the section that separates a real business plan from a tax-style budget. It shows the bank not just where you are today, but where you expect to be after the capital expenditure, the land purchase, the next season of debt reduction, or whatever decision the plan is built around.

A 5-year forecast does not need to be precise to be useful. The point is to lay out the trajectory: are you growing equity, reducing debt, maintaining liquidity? Is profit trending up, flat, or down? Are your key ratios moving in the right direction? Banks understand that year-five numbers are estimates. What they want to see is that you have thought through the path.

6. Risk Analysis and Scenarios

The section most farmers skip and the section banks most want to see. Risk analysis covers the major risks the business faces (seasonal, price, interest rate, regulatory, succession, biosecurity) and what you have planned to manage each one. Scenario analysis takes the most important risks and quantifies them: what does our cash flow look like if it rains 30% below average, if wheat drops to $250/t, if interest rates rise another 1%?

As our land purchase framework shows, modelling a few well-chosen scenarios is one of the most powerful things you can do in any plan. It demonstrates that you have stress-tested the business and know which combinations of conditions create real problems versus which are manageable. A bank reviewing two similar plans will always favour the one that shows the borrower has run the bad-case scenarios and has a response.

7. Goals and Milestones

The plan finishes with the goals the business is working toward and the milestones that mark progress. These should be specific and measurable: reduce debt by $300,000 over three years, lift equity ratio from 72% to 80% by 2028, transition 50% ownership to the next generation by 2030. Vague goals like "improve profitability" do not give you or your bank anything to track against.

As we covered in our farm business journey article, goals only become real when you write them down, attach numbers to them, and review progress regularly. The plan is the place to make them official.

What Banks Want to See vs What Most Farmers Submit

Talk to rural banking managers and the same complaints come up repeatedly. The plan is too short, too vague, and too historical. It shows last year's tax-style P&L without forward projections. It lists assets without current valuations. It mentions risks without quantifying them. The financial forecast is one column of optimistic numbers with no working assumptions visible.

What banks actually want is straightforward. They want a current balance sheet with realistic valuations. They want a monthly cash flow projection that shows how seasonal swings will be funded. They want a 5-year forecast with the assumptions visible (commodity prices, yields, interest rates) so they can test whether your numbers are reasonable. They want at least two scenarios run: a base case and a stressed case showing what happens if conditions deteriorate.

Tony Hudson's experience, covered in our securing farm finance article, illustrates the value of arriving at a bank review prepared. By presenting a complete, current plan with stress-tested forecasts, Hudson negotiated $15,000 a year off his interest costs - not because his business changed, but because the quality of his presentation changed how the bank assessed his risk.

The pattern is consistent. Better plans get better terms. Better terms compound over years. The hour spent preparing the plan properly is one of the highest-return uses of management time on most farms.

How P2PAgri Generates Most of These Sections Automatically

Building a business plan from a blank page is daunting, which is one reason so many farmers never start. The leverage point is to use a platform that pulls your accounting data into the right structure automatically, leaving you to focus on the assumptions, the strategy, and the narrative.

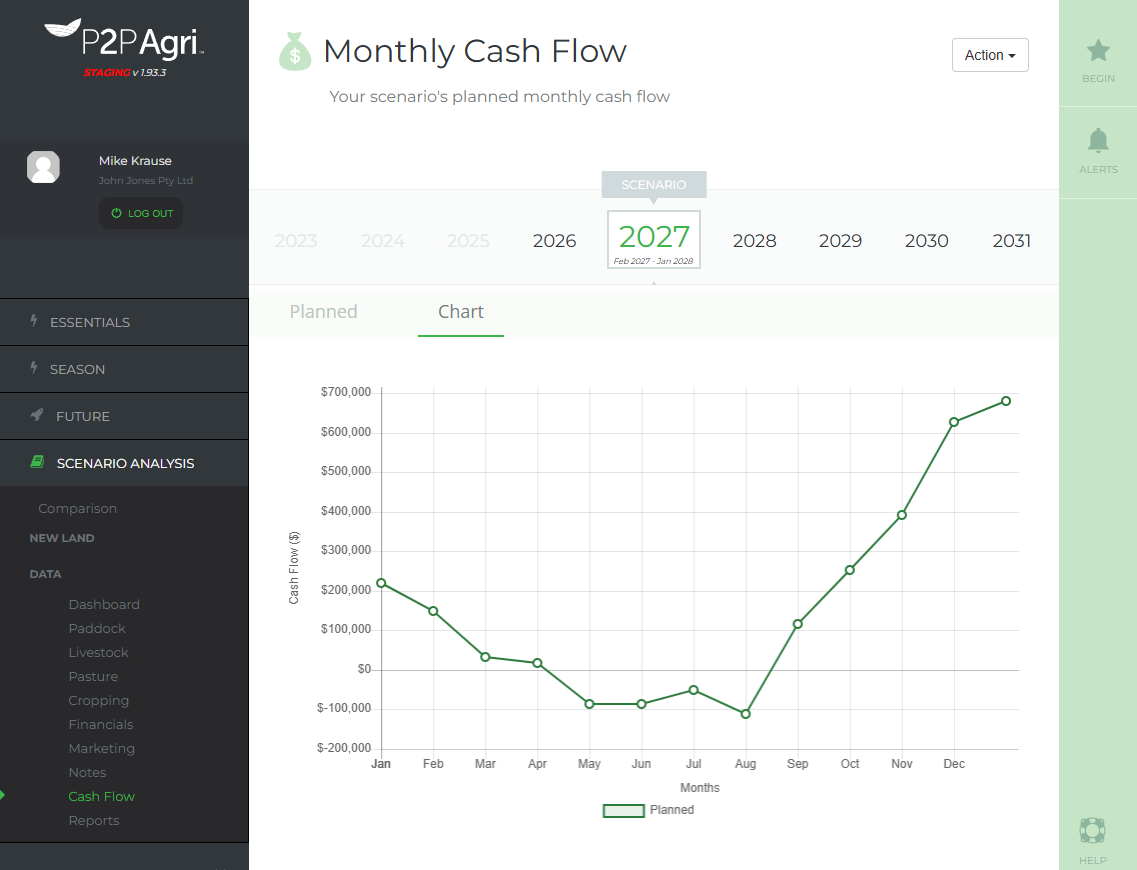

P2PAgri's farm business planning software generates the financial position, cash flow projection, 5-year forecast, and key ratios directly from your Xero data. The accounting transactions you already record become a Management P&L, Balance Sheet, Cash Flow projection, and Bank Ratio dashboard without you rebuilding them in a spreadsheet.

For the forward-looking sections, P2PAgri's Season and Future plans let you build enterprise budgets, project five years ahead, and run multiple scenarios side by side using Scenario Analysis. The narrative sections (executive summary, business overview, goals) you still write yourself, but the financial heavy lifting is done for you and stays in sync as the season progresses.

The point is not that the software writes your plan. The point is that it removes the tedious assembly work, so the time you spend on the plan is spent on the questions that actually matter: what are we trying to achieve, what could go wrong, and what are we going to do about it?

Example: A Business Plan Structure for a 2,000-Hectare Mixed Farm

To make this concrete, here is what the structure of a complete plan looks like for a hypothetical mixed cropping and livestock operation. Use it as a template to adapt for your own business.

Executive Summary (1 page). Smith Family Farms is a 2,000-hectare mixed enterprise in the SA Mid North, owned through a family partnership. The business runs 1,400 hectares of cropping (wheat, barley, lentils, canola) and 600 hectares supporting 2,500 first-cross ewes. 2024-25 net profit was $480,000 with an equity ratio of 78%. We are seeking a $1.5M term facility to fund the purchase of 400 neighbouring hectares, lifting forecast 5-year average profit by $145,000 per year.

Business Overview (2 pages). Ownership structure, key personnel (John and Mary Smith as principals, son Tom transitioning in over 5 years), location and rainfall (450mm long-term average), full enterprise breakdown, machinery and infrastructure summary, off-farm investments, and current succession status.

Financial Position (3-4 pages). Current balance sheet with land at independent valuation ($14M), plant and equipment at written-down value ($1.8M), livestock and grain on hand ($720,000), total debt schedule (one $850k mortgage at 5.4%, one $400k overdraft at 6.8%), key ratios with traffic-light assessment.

Cash Flow Projections (2 pages). Monthly cash flow for the 2026-27 season showing the seasonal pattern, peak finance requirement of $640,000 in October, and closing balance trajectory.

5-Year Forecast (3 pages). Projected P&L, balance sheet, and cash flow through 2030-31, including the impact of the land purchase from year two. Assumptions clearly stated: wheat at $310/t, barley at $280/t, canola at $720/t, lamb at $7/kg cwt, average yields based on 5-year farm history, interest rates assumed flat at current levels.

Risk Analysis and Scenarios (2-3 pages). Major risks identified and discussed: drought (mitigated by diversification and $300k cash reserve), commodity prices (mitigated by forward selling 30% of expected production), interest rates (stress-tested at +1% and +2%), succession (5-year transition plan documented). Three scenarios modelled: base case, dry-season case (yields 30% below average), price shock case (commodity prices 20% lower).

Goals and Milestones (1 page). Reduce non-mortgage debt to zero by 2028. Lift equity ratio to 82% by 2030. Complete 50% ownership transition to Tom by 2029. Achieve $200/ha 5-year average operating profit margin. Each goal with specific dates and tracking method.

Total: 14-16 pages. Built from data already in your accounting system, with the strategic sections written in plain English. This is a plan a bank will engage with, an adviser can use, and the family can review at annual meetings.

Common Mistakes That Weaken Farm Business Plans

Most plans that fail to impress fail for predictable reasons. Knowing the common mistakes helps you avoid them.

Too vague. Plans full of phrases like "we will improve productivity" or "we aim to grow the business" without numbers, timeframes, or actions. A plan needs measurable targets and specific actions, not aspirations.

Too optimistic. Plans built on best-case yield assumptions, peak commodity prices, and favourable seasonal conditions. Banks see straight through this. A plan that uses 5-year average yields and conservative price assumptions will be taken more seriously than one that needs everything to go right.

Missing scenario analysis. The plan presents one version of the future. No stress test, no alternative scenarios, no acknowledgment that things could go differently. This is the single biggest weakness in most plans, and the easiest to fix using Scenario Analysis.

Stale balance sheet. Land carried at a 2015 valuation, plant and equipment at original purchase price, livestock numbers from the last stocktake two years ago. Current valuations matter, particularly when land values have moved as much as they have.

No working assumptions. The 5-year forecast appears as a column of numbers with no visible explanation of where they came from. A reader cannot test the plan without knowing what commodity prices, yields, or input costs underpin it.

Built once, never updated. The plan was perfect when it went to the bank in March, but conditions changed and it was never revised. A plan that is more than 12 months old, or that does not reflect the current season, has lost most of its value as a management tool.

Where to Get Help Building Your Plan

You do not have to build a business plan alone. There are several good resources and supports available to Australian farmers in 2026.

P2PAgri advisers. The P2PAgri network includes qualified farm business advisers who work with you to build the plan using the platform, with the Management P&L, Balance Sheet, Cash Flow and 5-year forecast generated from your data. This combination of software and adviser is the fastest way to a complete plan.

Plan to Profit course. P2PAgri runs the Plan to Profit training program, which walks you through the principles in this article using your own farm numbers. Farmers who complete the course finish with a working plan they have built themselves.

Farming the Business manual. The free Farming the Business manual developed by Mike Krause for GRDC remains the most comprehensive reference for the financial principles behind a farm business plan. It covers cost of production, gross margin analysis, budgeting, and sensitivity analysis in detail.

RIC and government resources. The Regional Investment Corporation publishes guidance for farmers preparing applications for concessional loans, including business plan requirements. State agriculture departments also offer farm business management programs and grants for professional planning support.

Your accountant and lender. Both should be willing to review your draft plan and tell you what is missing from their perspective. The plan you send to your bank is more likely to land well if your bank manager has been part of the conversation along the way.

Build Your Plan This Month, Not Next Year

The best time to build a farm business plan was when you started the business. The second best time is this month. The next bank review, land purchase opportunity, succession conversation, or season change will be easier to navigate with a current plan than without one.

Start your free P2PAgri trial and connect your Xero data. Within minutes you will have your Management P&L, Balance Sheet and key bank ratios generated automatically. From there, build out your Season plan, model your 5-year forecast, run a couple of scenarios, and write the narrative sections in plain English.

Download the free Farming the Business manual for the underlying framework on cost of production, gross margins, and sensitivity analysis. Combined with the platform, you have everything you need to build a plan your bank will engage with and your business will actually use.

Put This Into Practice

P2PAgri helps you apply these concepts with interactive tools and real-time analysis of your farm data.

Get Started Free