Expand Your Farm Business or Invest Off-Farm? Compare for Profitability

There is no substitute for undertaking a professional approach to farm business analysis.

There are positive options when deciding whether to expand your farm business through land purchase, land leasing and share farming, or instead investing off-farm. The key is, however, to undertake the correct analysis so the whole farm performance of liquidity, efficiency and wealth is understood. This will ensure sound decision making and improved risk management.

Good, sound farm business analysis isn't always easy, but it can be done using improved analytic technology, and is worth doing.

Do this for yourself or use a professional farm business management consultant.

How do you choose the best strategy to expand your farm business wealth?

Farming has become more challenging with significant variation in seasonal outcomes, market volatility, increasing land values and tightening financial requirements from banks. The risks of farming are high. These conditions have made it challenging to know if all your financial resources should be placed back into the farming business or diversified into other investments. It is inevitable that the answer to these questions will be subjective – to make the perfect decision we would need to know what the future will be, which we don't! However, there are some fundamental principles that can be used to improve the decision-making process.

This paper outlines these principles and provides a farm case study to compare strategies to expand your farm business. Doing these analyses on your own farm business will allow you to compare these strategies with potential off-farm investment opportunities to maximise profitability.

Check list for the decision making process

Making decisions with uncertainty can be challenging but the following steps will help improve your decision-making to make the most of your opportunities. They will help you compare strategies to expand your farm business for improved financial outcomes.

1. Know the vision for your business

Knowing what business goals you wish to achieve in 10 years will greatly inform the decision to expand your farm business or diversify your investment. For example:

- Family Succession – Do you wish to expand your farm business to assist with the family succession? If this is the case, your goal should consider farm size to maintain its viability into the future.

- Retirement – Do you wish to expand your farm business to fund your retirement as there will be no next generation on the farm? In this case, you will be more concerned with the potential returns you can achieve from a wide range of investments.

- Risk – Are you concerned about the risks in agriculture and are looking for diversification to help manage that risk? In this case, diversifying your investments may be important to you.

(Check out Section 4 of ‘Farming the Business’ manual)

2. Know your passion

There is a great saying, ‘Do what you do, do best’! In other words, you will be willing to put in the extra effort needed for success if you love what you do.

If you love farming, you will manage your business well, which will likely mean your best return will be obtained when you expand your farm business.

If you are considering diversifying your investments off-farm, then consider if this is part of your passion. If you are not willing to learn about managing your investment off-farm and putting time and effort into this, then any gains you make could be absorbed by the investment costs you may incur. Be careful when deciding where to place your off-farm investment as it will need management.

3. Understand the three levels for good farm business management

When managing your business, it is helpful to plan and monitor these three aspects of your farming business (Section 3 of ‘Farming the Business’):

a. Liquidity – This is the cash flow of the business. A monthly planned and monitored cash flow budget greatly improves the business cash performance. If you are considering off-farm investment, also consider the cash flow implications to your whole business if you were to take cash out for an off-farm investment.

b. Efficiency – One of the key measures of financial performance is how well you have used the resources in your business, as measured by:

- Return on assets managed – This is the measure of how efficiently the total business assets are being managed. Total business assets include the value of owned, leased and share farmed land, machinery, water rights and livestock. When you are considering whether to expand your farm business, this measure assesses if it is a good use of your money. If your business doesn't improve in efficiency even with further investment, then you should perhaps put your money elsewhere. Knowing your efficiency is a key analytic to help you decide where your surplus money should be going.

- Return on Equity – This is the return you are getting from the assets you own, otherwise known as your equity. This is another key measure when deciding whether to invest off-farm. If your business is generating a 4% return on equity whereas a risk-free bank deposit would return 1%, then you would get better returns investing in your business. Do you know your business' return on equity?

If you wish to know more about these measures, refer to Section 5.5 of ‘Farming the Business’.

c. Wealth – This is measured by the business balance sheet and is known as Net Worth. Net Worth is the difference between the Total Assets owned and the Total Liability owed. This is the key performance indicator we wish to see grow over time. Further discussion of Net Worth is given in Section 5.3 of ‘Farming the Business’. Any investment consideration, whether to expand your farm business or invest off-farm, should be assessed for its likely impact on the Net Worth.

Farmers often ask ‘Why do I need to know my balance sheet, as I'm not going to sell the farm?’ It's not just about selling the farm – knowing your Net Worth is part of a risk management strategy as the higher the wealth in your business, generally the better risk is being managed. Also, banks place significant value in knowing your business balance sheet and the equity.

4. Do your analysis

Once you understand how to measure these three important measures of business liquidity, efficiency and wealth, you can apply them to any investment opportunity, both on-farm and off-farm. This helps you determine the best strategies to expand your farm business wealth.

You can do this yourself by studying the GRDC manual ‘Farming the Business’ or build a series of Excel spreadsheets. Or you can use the new, easy to use farm management modelling platform called ‘P2PAgri’.

Or you can use an experienced farm business management consultant. Some of these consultants are also found on the P2PAgri website find advisers

5. Make your decision

Despite having done significant business analysis, some people may find it difficult to make a decision. The biggest risk is actually not making any decision. Do the analysis, weigh up all the benefits and costs, decide on the best action, then follow through and act on that decision.

6. Communicate your decision to your partners

Once the decision is made, you will need to communicate this clearly with your business partners, if they haven't already been included in the decision-making process. This may also include your bank if you require additional finance.

For example, communicating clearly with your bank means they will be better informed of your business direction, and will gain the understanding and confidence they need to further invest in your business. Putting a professional document together supporting your decision and providing the bank with clear information they need could significantly decrease your risk grading and therefore decrease the interest rate you are offered (Check out Section 6 of ‘Farming the Business’).

While it's good to get the bank's approval on any new funding proposal you put to them, do not rely on their approval to gain confidence in your decision. Banks have a different goal in lending to you than you have for running your business. They will be making decisions on your business based clearly on their goals, not yours.

Some observations of the economy that affect business expansion

Two significant issues have helped shaped the rural economy in recent times:

- The increase in land values

- The cheapness and availability of finance

Land Values

Land values have been significantly increasing across the Australian agricultural landscape. This increase has been steady since 2000 and has been despite significant variability in the annual financial performance of different farming regions. For example, the Wimmera region of south-west Victoria appears to have experienced a 6% annual increase in value (Australian Farmland Values 2017, Rural Bank). Figure 1 indicates the average annual increase in land value in Victoria from 2012 to 2017.

Figure 1: Land Value increases from 2012 – 2017

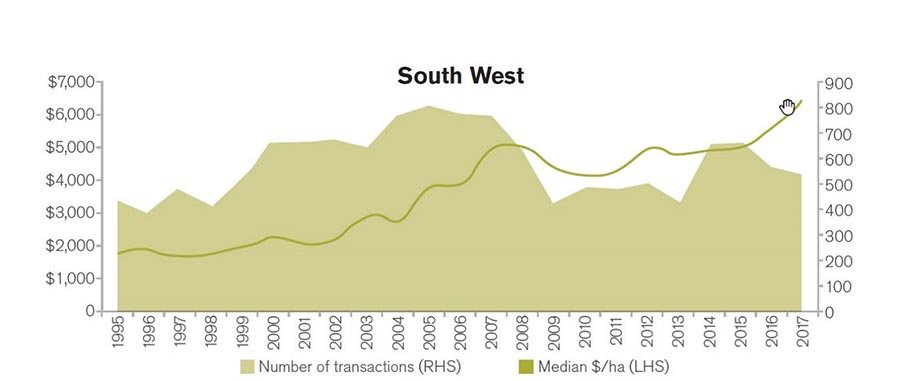

The trend in land values from 1995 in Victoria's South West is shown in Figure 2 and indicates a steady increase. This analysis comes from Australian Farmland Values 2017, Rural Bank.

Fig. 2 Land Value trends in Victoria's South-West

This land value increase has provided both benefits and costs:

Benefits

- The value of land in the farmer's balance sheet has significantly increased, adding directly to improved farm business net worth. Another way to look at this is that the wealth of the business has increased despite the financial performance of the business.

- As banks take security of their lending against the land value, they have felt financially secure with their rural lending, even through poor financial years. This has provided significant security for farming businesses through this period.

- Farmers have found it relatively easy to secure added finance when they have needed it.

Costs

- When farmers look to expand their business through additional land purchase, they have been paying these high land values and therefore must carefully consider the financial benefit of paying high prices for land.

- New entrants into farming have been greatly restricted as significant capital is needed to purchase land to start a farming business.

- It is challenging to achieve high Return to Assets Managed because the asset values are so high. This is why we have seen Australian farm businesses remain in family hands rather than corporate farming.

The Interest Rates

Historically, interest rates are at an all-time low. The RBA recently decreased the official rate to 1.00%. Figure 3 indicates the Reserve Bank of Australia's (RBA) official cash rates since 1989 and the trend has been significantly down.

Figure 3: RBA Cash Interest Rate

This has meant that the price of borrowing money is at very low levels. However, it must be noted that since the conclusion of the Royal Commission into Banking (Jan 2019), the access to new lending has become more difficult with significantly higher checking and data requirements. The approval time for new lending has significantly slowed. This means that farmers will need to become increasingly more professional in managing their relationship with their banks and in seeking more funding. Providing financial reports of you Liquidity, Efficiency and Wealth will significantly help demonstrate your business capacity to a bank.

It is observed that the recent experience of relatively cheaper lending could have been a major catalyst for the increase in farm land value, as farmers have been able to service more debt in their cash flow. Also during this time, banks were happy to lend interest only loans. However, recent bank lending is now swinging back more towards principal and interest lending (Amortised loans), where principal must also be repaid over time.

Buying vs leasing vs share-farming

This is the perennial question when it comes to how to expand your farm business. In the environment of increasing land values and low interest rates, should all expansion be land purchase?

Farmers rarely get the opportunity to assess all three options simultaneously when wishing to increase land area for their business. A Farm Case Study has been used to consider which option gives the best financial outcome, and demonstrates the process mentioned in points 3 and 4 above. While a typical mixed farm from the Lower North of SA with 2,000ha has been used in this analysis, the principles illustrated are applicable to all farm businesses. However, the results could be different when considering strategies to expand your farm business, so there is no substitute for undertaking you own proper analysis should you be considering these options.

The Farm Case-Study: Compare Options to Expand Your Farm Business

One way to assess the impact of an on-farm investment is to consider the following situation: you have just finished a great season and have $1m to invest and you wish to invest on-farm. You could:

- Purchase additional land

- Take on more land though leasing

- Take on more land through share-farming

The key characteristics of the Case Study farm, including the Enterprise details shown in Table 1, include:

- Land Area: 2,000 ha Av annual rainfall: 620mm 3 Labour units

- Equity 87%

- Total Asset Value: $25.5m

- Total Liability Value: $3.3m

Table 1: Case Study farm Enterprises, Yields and Rainfall Deciles

| Enterprises | Yields (t/ha) | Decile 3 Decile 5 Decile 7 |

|---|---|---|

| Barley | 175 ha | 3.5 5.0 6.0 |

| Wheat | 525 ha | 3.2 5.0 6.0 |

| Cereal hay | 300 ha | 5.0 7.0 10.0 |

| Canola | 280 ha | 1.2 1.8 2.2 |

| Faba beans | 420 ha | 1.5 3.0 4.0 |

| Pasture (Self-replacing Merino) | 300 ha |

The opportunity assessed is to add 300ha to the operation with the following characteristics:

- New land value: $5,000/ha with the same productivity as the home farm.

- Stamp duty of 5%

- Assume current labour and machinery will service the additional land

- Land use enterprises: 75ha each of wheat, hay, faba beans and canola.

The financial details of the new land options are shown in Table 2.

Table 2: Financial details of the three land options

| Land purchase | Land lease | Land share farmed |

|---|---|---|

| Put $1m into land purchase | $1m remains in bank | $1m remains in bank |

| Borrow $2.89m @ 5% | 300ha leased @ 5% of land value | 300ha agreement |

| Repay over 15 years | @75% income to the share farmer | |

| Assume a 5% annual growth in land values | @ 100% variable costs to the farmer |

The modelling was done using the new cloud based P2PAgri farm modelling software. As there are differences in risk between the land management options, an average season (Decile 5) was modelled in 2019, poor season (Decile 3) in 2020 and a good season (Decile 7) in 2021. The remaining three seasons of the 6-year planning period were left as average (Decile 5) seasons. This allows the risk profile of seasonal variation to be assessed between land purchased, land leased and land share farmed.

These three options are also compared against a ‘do nothing’ scenario. This is referred to as the FUTURE option on the following graphs.

The Farm Case Study Results

Liquidity

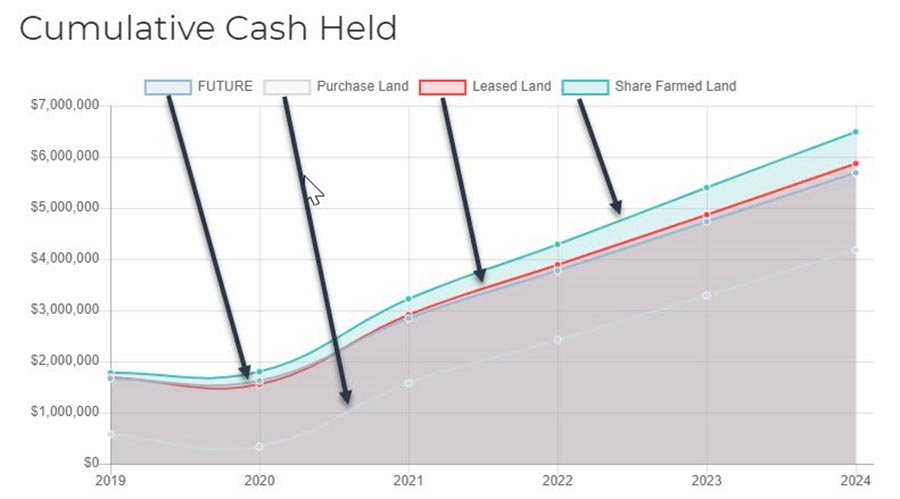

The cash surplus implications for the three options are shown in Figure 4. This modelling assumes that surplus cash is accumulated over the planning period. While this may not be the case as farmers have other uses for their surplus cash, it does illustrate which option generates the most cash.

Figure 4 shows that the share farming option provides to best opportunity to generate cash. This is related to the share farming agreement modeled of 75% of the income going to the farmer and the farmer paying 100% of the variable costs. The purchase of the 300ha of land showed the lowest accumulated cash as the $1m was used in the land purchase, and this loss of cash could not be caught up over this time period.

Figure 4: The modeled cash projections for each land option

Efficiency

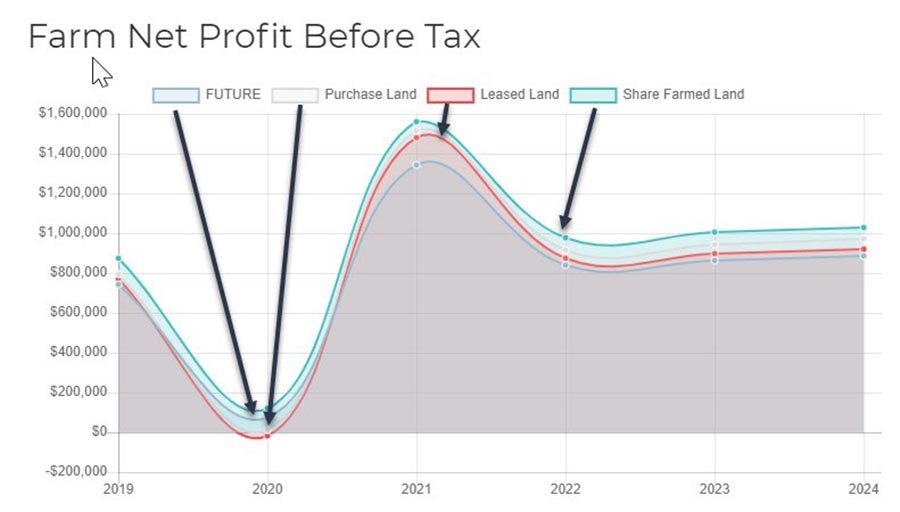

The addition of the 300ha does alter the risk profile of the business as shown in Figure 5. As expected, the financial performance is affected in the poor year of 2020, but great profits were generated in the better season projected in 2021.

This business is quite viable before the added land. Only the share farming option provided better profits in all seasons. Leasing and land purchase both produced less profit than ‘do nothing’ in the poor season of 2020, but both options generated improved profits compared to the ‘do-nothing’ in the projected good season of 2021.

Given average seasons, all options for taking on the added 300ha generated better profits than the ‘do nothing’ scenario.

Figure 5: The modeled Farm Net Profit before Tax

Return on Managed Assets is a sound measure for business efficiency and the results of the farm case study modelling are shown in Figure 6. The best results were the land purchase and land leasing. The ‘do- nothing’ and share farming options performed nearly identically but were not as good as the land purchase and land leasing options.

Figure 6: The modeled Farm Return on Assets Managed

Return to Equity is the best measure when comparing land expansion to off-farm investment. Table 3 shows the average estimated Return on Equity of the four farm options assessed. The results indicate the best Return on Equity was the share farming option.

The results compare favourably with the current bank deposit rate of 1% but are slightly lower than the average yield from the All Ordinary Equities of the last 5 years of 4%.

Table 3: The modeled Return on Equity

| Land Ownership Option | Average Return on Equity |

|---|---|

| Maintain the same land holding (Do nothing) | 2.99% |

| Purchase additional land | 3.15% |

| Lease additional land | 3.06% |

| Share farm additional land | 3.43% |

Wealth

Wealth is measured by the growth in Net Worth of the business and the projected Net Worth for all the options by 2024 is shown in Table 4. This indicates the best option is the land purchase. A land value growth of 5% has been assumed and the growth experienced on the value of land purchased was greater than the higher profits generated by the other options of leasing and share farming. So in this example, the best option to generate wealth is the land purchase option.

Table 4: The modeled final Net Worth

| Land Ownership Option | End of 6 years Net Worth |

|---|---|

| Maintain the same land holding (Do nothing) | $31.9m |

| Purchase additional land | $33.0m |

| Lease additional land | $32.0m |

| Share farm additional land | $32.5m |

Conclusion

The analysis of farm performance and assessing the options of land purchase vs leasing vs share farming is complex. However, if done correctly, it greatly informs the farm business decision-making. Doing this analysis may improve your credit risk rating with your bank and may result in obtaining a more favourable lending rate.

The Farm Case study analysis is provided to illustrate the detailed analysis needed to assess the various options to expand your farm business. If you are considering this option for your farming business, an analysis specific to your own business, opportunity and business environment is highly recommended. You can also utilise a qualified farm adviser to undertake this work for you.

This analysis does illustrate that in this lending environment of low interest rates and constant increasing land values, the land purchase option is viable and can improve efficiencies. However, this may not be the case for all land purchase opportunities and the business equity levels will have a significant effect on the analysis.

There is no substitute for undertaking your own analysis of your own opportunities.

The P2PAgri farm software provides a powerful toolbox to allow you to develop and compare your own scenarios. It allows you to do such things as plan for drought, buying land or extra farming equipment. Use 5-year financial projections to compare long-term profitability between expansion and off-farm investment options. If you would prefer help in developing these, access one of the P2PAgri Accredited Advisers on our website.

Put This Into Practice

P2PAgri helps you apply these concepts with interactive tools and real-time analysis of your farm data.

Get Started Free